Administrative fines in tax accounting. What account is attributed to the fine

- Rules for reflecting fines in accounting

- Reflection of penalties in tax accounting

- Assistance in drawing up contracts and maintenance of accounting

The reflection of fines in accounting is often problematic for an accountant. Fines, penalties and other penalties levied on an enterprise, as a rule, are associated with a penalty for violation of tax laws. Nevertheless, in the activity of any enterprise there may be situations when penalties are not related to the crime of the law.

One of the most common situations is non-compliance with contractual obligations of any of the parties, including the client or partner of the company. In this article, we will consider the rules for reflecting fines in accounting and tax accounting for breach of contract terms.

Rules for reflecting fines in accounting

The order of reflection of fines, penalties in accounting is governed by PBU 9/99 "Incomes of the organization" and PBU 10/99 "Expenses of the organization", approved by orders of the Ministry of Finance of the Russian Federation of 06.05.1999 (Nos. 32n and 33n, respectively).

According to regulatory documents, the amount of penalties paid to the company is referred to the “Other income” section. Consequently, the amount of compensation paid by the company belongs to the section “Other expenses”.

The cash paid is recorded in the financial statements by the following entry:

subaccount D 91-2 "Other expenses", K 76-2 "Settlements for claims" (amount) - payment by the company of penalties recognized by the court or organization.

The funds received are reflected as follows:

subaccount D 76-2 "Calculations for claims", K 91-1 "Other income" (amount) - amounts due to be received, recognized by the debtor or court,

where D is the debit of the account, K is the credit of the account.

Reflection of penalties in tax accounting

Reflection of fines , like any other expenses and income, affects the amount of taxable income. According to subparagraph 13 of paragraph 1 of Article 265 of the Tax Code of the Russian Federation, penalties caused by non-observance of contractual obligations recognized by the debtor or payable by court decision are included in non-operating expenses. Thus, taxable income is reduced.

According to clause 3 of Article 250 of the Tax Code of the Russian Federation, the compensation received by the company for fines refers to the composition of non-operating income. The amount of income tax will depend on the terms of the contract. If it contains a specific amount of payment for breach of obligations, the taxable profit increases.

Assistance in drawing up contracts and maintenance of accounting

Audit firm "Audit in business and finance" provides advice on any issues related to accounting and tax optimization. We render, we carry out, we are engaged in registration of all types of contracts.

Knowledge of the nuances of legislation and the ability to correctly formulate contractual obligations directly affect the success of your company. With the help of qualified lawyers and accountants you can foresee all problem situations, minimize and prevent possible penalties.

The normal activity of any enterprise implies the emergence of income, expenses, penalties. As a rule, when drawing up reports they refer to the necessary accounting items. However, even experienced accountants sometimes have questions about exactly where to apply fines, penalties and penalties, as there are some peculiarities. Let's deal with this in more detail.

First you need to figure out what are the fines, their types and procedure for regulation by the legislation of the Russian Federation. There are such types of sanctions:

- Fines of a civil law group (for example, for violation of contractual terms);

- Administrative penalties (here you can include fines in the tax service, traffic police, for litigation, extra-budgetary funds and other institutions, as well as violation of the deadline for providing information on a bank account).

A penalty, in contrast to a fine, arises when the payment of tax obligations to the treasury is not timely. Therefore, one should distinguish between these two concepts. In order to have an idea about the procedure for fees and their sequence, it is necessary to familiarize yourself with the provisions of the Tax Code (Section 4).

It is important to understand to which category a particular type of fine belongs for correct reflection in accounting. According to PBU 10/99 “Organization expenses”, all fines (as well as penalties and fines) are included in the item “Other expenses”. And their amounts reflected in the account are taken on the basis of court decisions, claims from organizations. It should be understood that the amount of fines of the company are not taken into account when taxing profits. Therefore, when summarizing and completing reports, they are not included in the income tax expense.

Now consider how this is reflected in accounting. As determined by the Chart of Accounts of the Russian Federation, all penalties are conducted through account 68 (settlements on taxes and fees). As a rule, correspondence is applied to the account 99 "Profit and loss" using various subaccounts for certain types of penalties. For example, if an enterprise was supposed to pay tax on November 5, and did it on the 30th day of the next month, the resulting penalty amount in the amount of 1000 rubles is reflected as follows:

- We charge the amount of interest: Debit 99 (sub-account “Penalty”) Credit 68 - in the amount of 1000 rubles;

- Enumerate the amount of interest in the budget: Debit 68 Credit 51 - in the amount of 1000 rubles.

Download from us on the portal:

Consider one of the most common cases of the occurrence of a penalty - violation of the timing of notification of the tax service of opening (or closing) bank accounts. For example, according to Article 118 of the Tax Code of the Russian Federation, a fine was imposed on an enterprise for this reason in the amount of 3,000 rubles. Then the entries are made as follows:

- Dt 99, sub-account “Penalty” Kt 68, sub-account “Penalty” - a sanction was taken into account in the amount of 3,000 rubles;

- Dt 68, subaccount "Penalty" Kt 51 - a fine paid to the state treasury.

By the same principle, postings are made when sanctions are transferred to extra-budgetary funds, which is also not taken into account in the amount of taxable income.

Download from us on the portal.

If the company violates the terms of the contract with the counterparty, it becomes necessary to pay a penalty, which is determined by the provisions of the Civil Code of the Russian Federation. This may occur:

- If the deadlines for the fulfillment of obligations are violated;

- Simple happened vehicle (in the case of shipment);

- Violated the terms of payment, etc.

In tax accounting, these penalties relate to non-operating expenses (or income). In accounting, they are included in the article "Other expenses". For the postings used accounts: 91 (income, expenses) and 76 (relations with counterparties). In this case, various subaccounts are usually applied.

Download right now:

Unfortunately, very often when conducting business, there are cases of breach of obligations to suppliers or tax agents. In this case, the management of the enterprise should pay attention to this to eliminate the possibility of their recurrence. And the most important thing is to correctly conduct all the accounts and reflect in the financial statements. The above instructions will help you in this difficult matter!

After checking by the labor inspectorate, an administrative fine of 50,000 rubles was imposed. on the organization as a legal entity and 3000 rubles. on the director of art. 5.27 Administrative Code. The amount of 50 000 rubles. was paid from the current account of the organization. The director decided to voluntarily recover from his salary the fine imposed on the organization in the amount of 50,000 rubles.

As an organization, consider the amount of the paid and reimbursed fine in the amount of 50,000 rubles. in accounting and tax accounting?

Having considered the issue, we came to the following conclusion:

If the director of the organization decided to voluntarily refund the amount administrative fine imposed on the organization, the organization should, on the date of making such a decision, reflect other income in accounting, and recognize non-operating income in tax accounting.

Rationale for the withdrawal:

Legal entities are subject to administrative liability for committing administrative offenses in cases provided for by the articles of Section II of the CAO RF or by the laws of the subjects of the RF on administrative offenses (CAO RF).

The amount of the administrative fine shall be credited to the budget in full in accordance with the legislation of the Russian Federation (CAO RF).

Accounting

Provisions on accounting It is not determined what expenses include the costs of paying fines administrative offenses . Obviously, they do not meet the cost criteria for ordinary activities (pp. 4, 5 "Expenditures of the organization"). Therefore, these expenses should be considered as part of other expenses on the basis of paragraph 12.

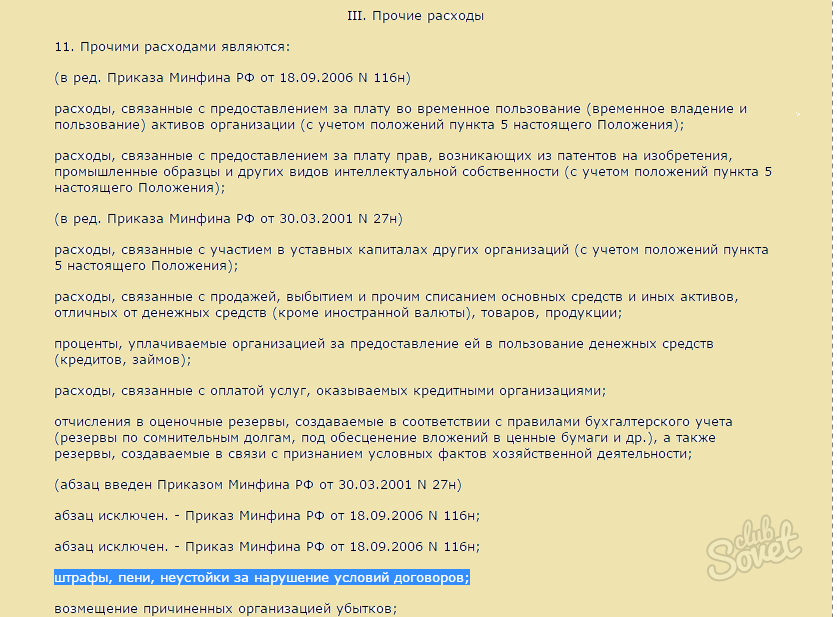

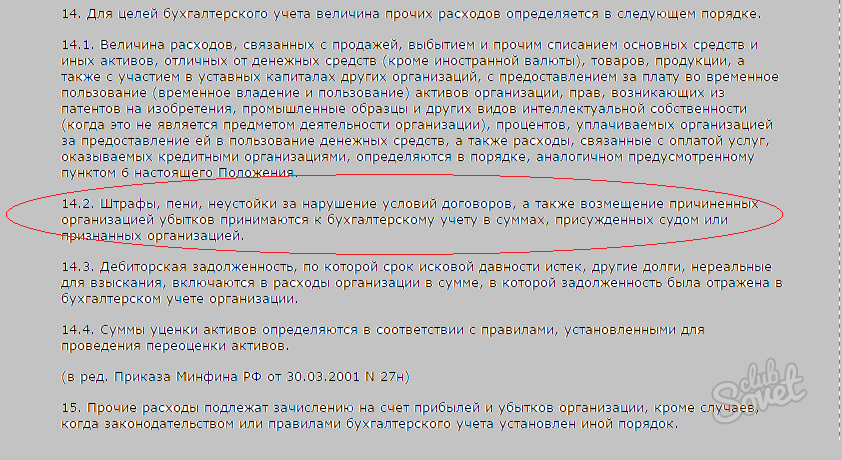

On the basis of clause 14.2, fines, penalties, and penalties for violation of the terms of contracts, as well as compensation for losses caused by the organization are accepted for accounting in the amounts awarded by the court or recognized by the organization.

Note in accordance with the Instructions for the application of the chart of accounts for financial accounting and financial activity of organizations approved by the Ministry of Finance of Russia dated October 31, 2000 N 94n (hereinafter referred to as the Instructions), the list of expenses reflected in account 99 "Gains and losses" is closed. From the list provided in the Instruction, only sums of tax sanctions are counted for account 99.

At the same time, the Instruction for the compilation of information on other incomes and expenses of the reporting period provides for the account 91 “Other income and expenses”.

Considering the above, we believe that operations related to the accrual and payment of an administrative fine by the organization are reflected in the accounts as follows:

Debit 91, subaccount "Other expenses" Credit 76, subaccount "Calculations for administrative fines"

- 50 000 rub. - an administrative fine has been charged;

Debit 76, subaccount "Calculations for administrative fines" Credit 51

- 50 000 rub. - An administrative fine is transferred to the budget.

If the director of the organization decides to voluntarily reimburse the amount of the administrative fine imposed on the organization, then the organization should take the amount of the compensation to other income. This compensation is not related to the proceeds from the sale of products (goods, works, services) (Clauses 2, 4, 5, "Incomes of the organization").

According to clause 10.2, fines, penalties, and penalties for breach of the terms of contracts, as well as compensation for losses caused to the organization, are accepted for accounting in the amounts awarded by the court or recognized by the debtor. At the same time, in accordance with paragraph 16, such receipts are recognized in accounting in the reporting period in which the court made a decision on their recovery or they were recognized by the debtor.

Thus, if the director decided to voluntarily reimburse the amount of damage (fine), then the other income in the form of the amount of compensation is recognized on the date of its recognition (the adoption of such a decision).

The instruction provides that on subaccount 73-2 "Calculations for compensation for material damage" of account 73, calculations for compensation for material damage caused by an employee of the organization as a result of shortages and theft of cash and inventory, marriage, and also for other types of damage are taken into account .

Thus, we believe that in this case the following entries should be made in the accounting of the organization:

Debit 73, subaccount "Calculations for compensation of material damage" Credit 91 "Other income"

- reflects the director’s indebtedness on the reimbursement of an administrative fine on the basis of the decision;

Debit 70 Credit 73, subaccount "Calculations for compensation for material damage"

- amounts withheld from salary director.

Tax accounting

On the basis of the Tax Code of the Russian Federation, when determining the tax base for the tax on the profit of organizations, in particular, expenses in the form of fines, fines and other sanctions transferred to the budget (to state extrabudgetary funds), and interest payable to the budget in accordance with the Tax Code of the Russian Federation as well as fines and other sanctions levied by government organizations that are granted the right to impose the sanctions by the legislation of the Russian Federation.

Consequently, the costs of the payment of administrative fines under the act of verification labor inspection when calculating the tax base for income tax, they are not included in expenses due to the direct prohibition established by the Tax Code of the Russian Federation (see also the Ministry of Finance of the Russian Federation of 12.03.2010 N 03-03-06 / 1/127, UFNS for Moscow of 22.12.2005 N).

As for the director’s reimbursement of the amount of the administrative fine paid, we would like to draw attention to the fact that, on the basis of the RF Tax Code, non-operating income of a taxpayer is recognized, in particular, income in the form recognized by the debtor or payable by the debtor on the basis of a court decision that entered into legal force, fines, penalties and (or) other sanctions for violation of contractual obligations, as well as the amount of compensation for loss or damage.

The date of receipt of this type of income in the application of the accrual method is the date of recognition by the debtor or the date of entry into force of a court decision (NK RF).

Thus, if the director of the organization decides to voluntarily reimburse the amount of the administrative fine, the organization will have to recognize non-operating income on the date of such a decision.

The answer is prepared:

Expert Advisor Legal Consulting GARANT

auditor, member of the Russian Board of Auditors Liliya Fedorova

The answer passed quality control

The material was prepared on the basis of individual written advice provided within the framework of the Legal Consulting service.

In accounting and tax accounting?